David Carboni makes a great point in this piece: successful powerhouse businesses, paragons of scaling up (your Netflixes, Googles, Ubers, et al), could never build the disruptive, fast-moving products that made them successful from their positions today:

Admired and respected as towering giants of our digital world, our hero companies emanate an almost mythical quality. The scale, power and inspiration they command are the stuff of legend. Glib statements about “business” distort their stories into gaudy two-dimensional caricatures whilst organisations seeking Digital Transformation aspire to emulate what they see in this theatre. Paradoxically our heroes would be the first to point out they wouldn’t be able to build themselves as they stand today.

So much of what’s required to actually scale to Google or Netflix level is fundamentally unknown and actually nonexistent when they ran into their scaling frictions. Due to their unique needs to deliver their products to hundreds of millions of simultaneous users, Netflix builds Chaos Monkey, Google creates Kubernetes. There’s nothing wrong with these tools; they solve problems that are nearly one-of-a-kind for businesses that are in a class of very few.

The envy of their ability to scale, and an overconfidence that “I’ll need this one day, too”, tempts startups to build for scale way too early. But the cause-effect on their success is misattributed. These megascalers didn’t get to hypergrowth because they built deployment automations, CI/CD magic, or microservice‘d their architecture. They did those things because their early quick-and-dirty, unscalable experimentation helped them find generational product-market fit first.

From where they sit today, their inventions for scale would be active impediments to disruptive innovation.

Success is a messy business, exploratory, trying, failing, scratching your head, learning something new, trying to think different.

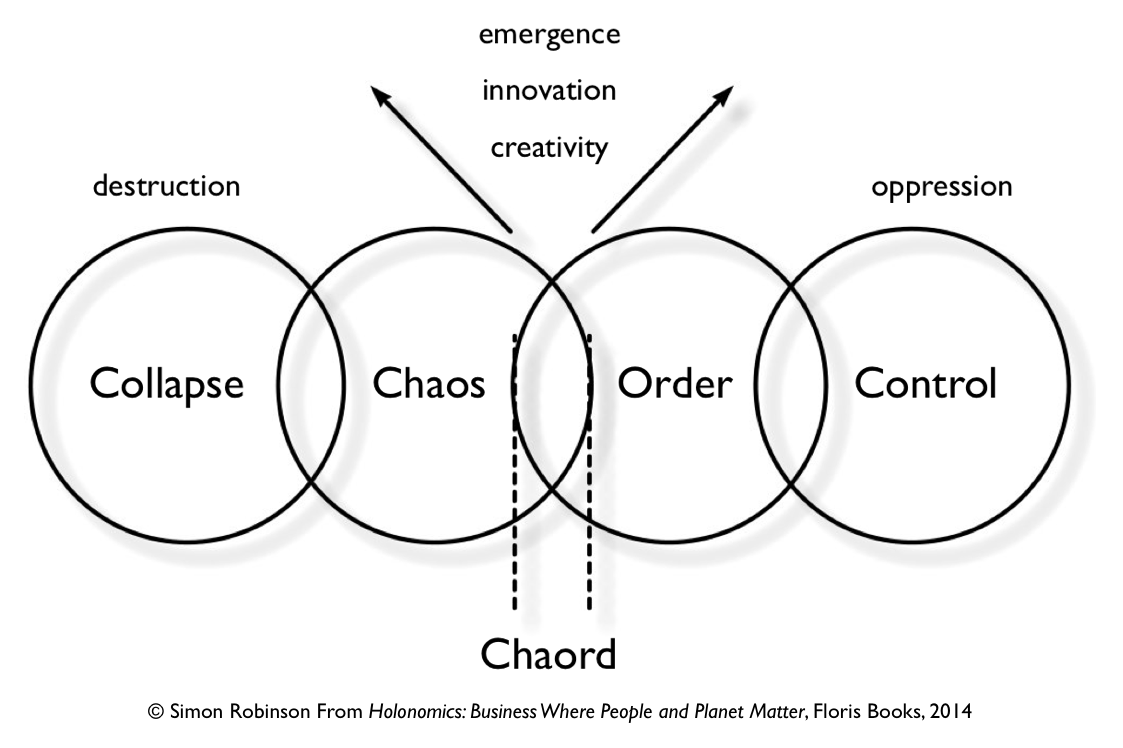

The late Dee Hock, founder of Visa, was a business legend in many respects. Like many of the most revered founders, his ideas were years ahead of their time, and his writing is clear, concise, and super interesting. He famously organized Visa around a decentralized management model, in an era when the norm was the extremely centralized, hierarchical structure. Companies like Amazon, Johnson and Johnson, Uber, Valve Software, and others have adopted the same principles Hock pioneered to make their companies more resilient in the face of challenge.

In 2000 he published a book called Birth of the Chaordic Age which described his thesis on systems that straddle a boundary between imposing order while embracing chaos — ”chaordic” systems. This essay sets out the central idea:

The production of goods and services has progressed from the Age of Hand-crafting through the Industrial Age, more accurately thought of as the Age of Machine-crafting, into the so-called Information Age, which can best be understood as the Age of Mind-crafting, (or as I prefer to call it, the Chaordic Age,) since information is nothing but the raw material of that incredible processor we call mind and the pseudo-mind we call computer.

The Age of Machine-crafting was primarily an extension of muscle power. The Chaordic Age is primarily an extension of mental power.

In the Chaordic Age, where innovation and successful “adaptation” requires the leverage of individual minds, organizations need to embrace individual intuition and judgment to keep up. In the past, the primary goal of a corporation was to encode processes and decision-making criteria into the corporate structure itself — to eliminate the need for any particular person, and make the human beings interchangeable equivalent parts. Hock says in the future, this model won’t work:

In organizations of the future the centuries-old effort to eliminate judgment and intuition, art if you will, from the conduct of institutions will change. Organizations have too long aped the traditional mechanistic, military model wherein obedience to orders is paramount and individual behavior or independent thinking frowned upon, if not altogether forbidden. It will be necessary at every level to have people capable of discernment, of making fine judgments and acting sensibly upon them.

He was onto something. Business schools need to catch up.

Geospatial analytics company Descartes Labs recently sold to private equity, in what former CEO Mark Johnson calls a “fire sale.” This post is his perspective on the nature of the business over time, their missteps along the way in both company identity and fundraising, and some of the shenanigans that can happen as stakeholders start to head for the exits.

Not knowing much about Descartes’ actual business, either the original vision of the product or its actual delivery over the years, I don’t have much specific perspective to offer. But this story is a recurring theme in the world of spatial, earth observation, and analytics startups that have come and gone over the past 10 years or so. These businesses are built on extremely capital-intensive investments in satellites, space-based sensors, and data, which are major hurdles that cause many of them to get sideways in their fundraising structures very early in their business journeys.

The early years of a startup are always extremely volatile, with pivots and adjustments happening along the way as the company navigates the idea maze, looking for product-market fit. I think the heavy capital required up front compels funders to expect too much too soon in the product development process. There’s a chicken-and-egg problem — the PMF search in these kinds of businesses costs many millions. If you’re building a SaaS project management tool, you can wander around looking for fit for years with only a few people and limited seed money. But in satellite startups, the runway you need to do product-market experimentation is enormously expensive. Large enough funding pools also saddle the business with aggressive expectations for customer counts, growth, and revenue. With revenue targets set but no repeatable PMF, many of these startups do whatever they can to find dollars, which often leads to doing what are effectively custom services deals for a single or few customers. That’s necessary to make money of course, and it’s not valueless for product validation. But it’s too narrow to function as true PMF. Stay in this awkward state too long and you end up stuck down the wrong hallways of the idea maze. You’ll never find the fitness you need to build a lasting business. Billwrote a great post on this recently, about this identity struggle between being a solutions, services, or product company.

The best thinking on the topic of EO and satellite data companies is my friend Joe Morrison’s newsletter, “A Closer Look”. He leads product for Umbra, a startup specializing in SAR. He’s done a lot more thinking than me on this topic and has thoughtful takes on the satellite and geo market in general.

Sam Gerstenzang wrote an excellent piece a couple weeks ago with operating lessons for growing companies, driven by his learnings from the product team at Stripe. Personally, I’ve got a decade or so of experience as an “operator” at a “startup” (two words I wouldn’t have used to describe my job during most of that time). Since 2011 I’ve led the product team at Fulcrum, a very small team until the last few years, and still only in the medium size range. So my learnings on what “good operating” looks like are based mostly on this type of experience, not necessarily how to lead a massive product team at a 10,000 person company. I think a surprising number of the desirable characteristics translate well, though. Many more than BigCo operator types would have you believe.

Overall this list that Sam put together is especially great for teams that are small, early, experimental, or trying to move fast building and validating products. There are a few tips in here that are pretty contrarian (unfortunately so, since they shouldn’t be contrarian at all) to most of what you’ll read in the literature on lean, agile, startuppy teams. But I like that many of these still apply to a company like Stripe that’s in the few-thousands headcount range now. There isn’t that stark a difference in desirable characteristics between small and large teams — or at least there doesn’t need to be.

On the desire to enforce consistency:

Consistency is hard to argue against – consistency reinforces brand and creates better ease of use – but the costs are massive. Consistency just feels good to our system centric product/engineering/design brains. But it creates a huge coordination cost and prohibits local experimentation – everything has to be run against a single standard that multiplies in communication complexity as the organization gets larger. I’d try to ask “if we aim for consistency here, what are the costs, and is it worth it?” I think a more successful way to launch new products is to ignore consistency, and add it back in later once the project is successful. It will be painful, but less painful than risking success.

I’d put this in the same category as feeling need to “set yourself up to scale”. When a team lead is arguing to do something in a particular way that conforms with a specific process or procedure you want to reinforce through the company, it’s an easy thing to argue for. But too often it ignores the trade-offs in coordination overhead it’ll take to achieve. Then the value of the consistency ends up suspect anyway. In my experience, coordination cost is a brutal destroyer of momentum in growing companies. Yes, some amount of it is absolutely necessary to keep the ship floating, but you have to avoid saddling yourself with coordination burdens you don’t need (and won’t benefit from anyway). Apple or Airbnb might feel the need to tightly coordinate consistency, but you aren’t them. Don’t encumber yourself with their problems when you don’t have to.

Enforcement of consistency — whether in in design, org charts, processes, output — has a cost, sometimes a high cost. So it’s not always worth the trade-off you have to make in speed or shots-on-goal. With a growing company, the number of times you can iterate and close feedback loops is the coin of the realm. Certain things may be so important to the culture you’re building that the trade-off is worth it, but be judicious about this if you want to maintain velocity.

On focus:

People think focus is about the thing you’re focused on. But it’s actually about putting aside the big shiny, exciting things you could be working on. The foundation of focus is being clear upfront about what matters—but the hard work is saying no along the way to the things that feel like they might matter.

True focus is one of the hardest parts once your team gets some traction, success, and revenue. It’s actually easier in the earlier days when the sense of desperation is more palpable (I used to say we were pretty focused early on because it was the only way to get anything made at all). But once there’s some money coming in, users using your product, and customers are growing, you have time and resources you didn’t have before that you can choose to allocate as you wish. But the thing is, the challenge ahead is still enormous, and the things you’ve yet to build are going to get even more intricate, complex, and expensive.

It’s simple to pay lip service to staying focused, and to write OKRs for specific things. But somehow little things start to creep in. Things that seem urgent pop up, especially dangerous if they’re “quick wins”. You only have to let a few good-but-not-that-important ideas float around and create feel-good brainstorming sessions, and before you know it, you’ve burned days on stuff that isn’t the most important thing. There’s power in taking an ax to your backlog or your kanban board of ideas explicitly. Delete all the stuff you aren’t gonna do, or at least ship it off to Storage B and get to work.

On product-market fit and small teams:

Start with a small team, especially when navigating product market fit. Larger teams create communication overhead. But more importantly they force definition = you have to divide up the work and make it clear who is responsible for what. You’re writing out project plans and architecture diagrams before you even should know what you’re building. So start small and keep it loose until you have increased clarity and are bursting at the seams with work.

To restate what I said above, it’s all about feedback loops. How many at-bats can you get? How many experiments can you run? Seeking product-market fit is a messy, failure-ridden process that requires a ton of persistence to navigate. But speed is one of your best friends when it comes to maintaining the determination to unlock the job to be done and find just enough product fit that you get the signals needed to inform the next step. Therefore, small, surgical teams are more likely to successfully run this gauntlet than big ones. All of the coordination cost on top of a big, cross-functional group will drain the team, and greatly reduce the number of plate appearances you get. If you have fewer points of feedback from your user, by definition you’ll be less likely to take a smart second or third step.

The responsibility point is also a sharp one — big teams diffuse the responsibility so thinly that team members feel no ownership over the outcomes. And it might be my cynicism poking through, but on occasion advocates for teams to be bigger, broader, and more cross-functional are really on the hunt for a crutch to avoid ownership. As the aphorism goes, “a dog with two owners dies of hunger.” Small teams have stronger bonds to the problem and greater commitment to finding solutions.

Overall, I think his most important takeaway is the value of trust systems:

Build trust systems. The other way is to create systems that create trust and distributed ownership – generally organized under some sort of “business lead” that multiple functions report to. It’s easier to scale. You’ll move much more quickly. A higher level of ownership will create better job satisfaction. But you won’t have a consistent level of quality by function, and you’ll need to hire larger numbers of good people.

A company is nothing but a network of relationships between people on a mission to create something. If those connections between people aren’t founded in trust and a shared understanding of goals and objectives, the cost of coordination and control skyrockets. Teams low in trust require enormous investment in coordination — endless status update meetings, check-ins, reviews, et al1. If you can create strong trust-centric operating principles, you can move so much faster than your competition that it’s like having a superpower. The larger teams grow, of course, the more discipline is required to reinforce foundations of trust, but also the more important those systems become. A large low-trust team is incredibly slower than a small one. Coordination costs compound exponentially.

Don’t take this to mean I’m anti-meeting! I’ve very pro-meeting. The problem is that ineffective ones are pervasive. ↩

A classic from Mark Suster on patience and pattern recognition for investors:

The first time I meet you, you are a single data point. A dot. I have no reference point from which to judge whether you were higher on the y-axis 3 months ago or lower. Because I have no observation points from the past, I have no sense for where you will be in the future. Thus, it is very hard to make a commitment to fund you.

For this reason I tell entrepreneurs the following: Meet your potential investors early. Tell them you’re not raising money yet but that you will be in the next 6 months or so. Tell them you really like them so you want them to have an early view (which is what all investor’s want). When you’re with them lower the bar by telling them, “we haven’t shipped product yet, we have lots of decisions still to make, but we’d like to show you our prototype” or obviously if you’re more advanced show what you have and what your roadmap looks like.

Because early-stage investing is such a long relationship game, this view seems obvious. But people still make snap decisions to jump into deals (both investors AND startups) based on who’s hot or who’s trendy, which they have little empirical evidence on performance, grit, commitment to do what they say, and other important data points.

The construction market for startups (one that I’m fairly involved in, but only as a segment of our market) has been a historically tough nut to crack for technology companies.

This is a great breakdown from Brian Potter on the past couple decades of construction startups and funding amounts, with a useful segmentation by category into slices like builders, materials, energy use, construction software, digital twins, and more.

It wasn’t surprising to see builders taking such a huge proportion of the funding — after all, trying to scale a soup-to-nuts homebuilding company is enormously capital-intensive. Management software scoops in an ~8% share, with Procore at the top. This bit hits on one of the challenges I’ve observed anecdotally working with construction companies: a slog to scale within big orgs due to various reasons:

Most VC returns come from a small number of huge successes that end up being worth 10s or 100s of billions (for instance, 65% of the value of YCombinator startups comes from just 5 companies), but construction has yet to see any $10 billion+ startups. Part of this is possibly due to a sort of natural throttling (caused by, among other things, rational risk aversion) that limits how fast even a software company with strong network effects can grow in construction. For instance, at its IPO, Procore estimated that it had captured just 2% of its potential market despite being around for over 15 years and having a category-defining product.

Some of the frictions are common in other markets, but particularly acutein construction — risk aversion, resistance to tech, and fragmented cost centers until you get to enterprise-scale (departments compete for their own revenue/budget, and the company wants to book software expenses as op-ex to a project). Plus the multiparticipant nature of every construction project (a sea of subs and contractors) makes it difficult to go upstream with a single stakeholder buyer.

If you’re on the internet and haven’t been living under a rock for the last few months, you’ve heard about the startup Clubhouse and its explosive growth. It launched around the time COVID lockdowns started last year, and has been booming in popularity even with (maybe in-part due to?) an invitation gate and waitlist to get access.

The core product idea centers around “drop-in” audio conversations. Anyone can spin up a room accessible to the public, others can drop in and out, and, importantly, there’s a sort of peer-to-peer model on contributing that differentiates it from podcasting, its closest analog.

I got an invite recently and have been checking out sessions from the first 50 or so folks I follow, really just listening so far. Their user and growth numbers aren’t public, but from a glance at my follow recommendations I see lots of people I follow on Twitter already on Clubhouse.

They recently closed a B round led by Andreessen Horowitz, who also backed the company in its earlier months last year. Any time an investor does successive rounds this quickly is an indicator of magic substance under the hood, signals that show tremendous upside possibility. In the case of Clubhouse, user growth is obviously a big deal — viral explosion this quickly is always a good early sign — but I’m sure there are other metrics they’re seeing that point to something deeper going on with product-market fit. Perhaps DAUs are climbing proportional to new user growth, average session duration is super long, or retention is extremely high (users returning every day).

On the surface a skeptical user might ask: what’s so different here from podcasts? It’s amazing what explosive growth they’ve had given the similarities to podcasting (audio conversations), and considering its negatives when compared with podcasts. In all of the Clubhouse rooms I’ve been in, most users have telephone-level audio quality, there’s somewhat chaotic overtalk, and “interestingness” is hard to predict. With podcasts you can scroll through the feed and immediately tell whether you’ll find something interesting; when I see an interesting guest name, I know what I’m getting myself into. You can reliably predict that you’ll enjoy the hour or so of listening.

Whenever a new product starts to take off like this, it’s hitting on some aspect of latent user demand, unfulfilled. What if we think about Clubhouse from a Jobs to Be Done perspective? Thinking about it from the demand side, what role does it play in addressing jobs customers have?

Clubhouse’s Differentiators

Clubhouse describes itself as “Drop-in audio chat”, which is a stunningly simple product idea. Like most tech innovations of the internet era, the foundational insight is so simple that it sounds like a joke, a toy. Twitter, Facebook, GitHub, Uber — the list goes on and on — none required invention of core new technology to prosper. Each of them combined existing technical foundations in new and interesting ways to create something new. Describing the insights of these services at inception often prompted responses like: “that’s it?”, “anyone could build that”, or “that’s just a feature X product will add any day now”. In so many cases, though, when the startup hits on product-market fit and executes well, products can create their own markets. In the words of Chris Dixon, “the next big thing will start out looking like a toy”.

Clubhouse rides on a few key features. Think of these like Twitter’s combo of realtime messaging + 140 characters, or Uber’s connection of two sides of a market (drivers and riders) through smartphones and a user’s current location. For Clubhouse, it takes audio chat and combines:

Drop-in — You browse a list of active conversations, one tap and you drop into the room. Anyone can spin up a room ad-hoc.

Live — Everything happening in Clubhouse is live. In fact, recording isn’t allowed at all, so there’s a “you had to be there” FOMO factor that Clubhouse can leverage to drive attention.

Spontaneous — Rooms are unpredictable, both when they’ll sprout up and what goes on within conversations. Since anyone can raise their hand and be pulled “on stage”, conversation is unscripted and emergent.

Omni-directional — Podcasts are one-way: from producer to listener, or some shows have “listener mail” feedback loops. Clubhouse rooms by definition have a peer-to-peer quality. They truly are conversations, at least as long as the room doesn’t have 8,000 people in it.

None of these is a new invention. Livestreaming has been around for years, radio has done much of this over the air for a century, and people have been hosting panel discussions since the time of Socrates and Plato. What Clubhouse does is mix these together in a mobile app, giving you access to live conversations whenever you have your phone plus connectivity. So, any time.

Through the Lens of Jobs

Jobs to Be Done focuses on what specific needs exist in a customer’s life. The theory talks about “struggling moments”: gaps in demand that product creators should be in search of, looking for how to fit the tools we produce into true customer-side demand. It describes a world where customers “hire” a product to perform a job. Wherever you see products rocketing off like Clubhouse, there’s a clear fit with the market: users are hiring Clubhouse for a job that wasn’t fulfilled before.

Some might make the argument that it’s addressing the same job as podcasts, but I don’t think that’s right exactly. For me it has hardly diminished my podcast listening at all. I think the market for audio is just getting bigger — not a zero-sum taking of attention from podcasts, but an increase in the overall size of the pie. Distributed work and the reduction of in-person interaction and events has amplified this, too (which we’ll get to in a moment, a critical piece of the product’s explosive growth).

Let’s go through a few jobs to be done statements that define the role that Clubhouse plays in its users’ lives. These loosely follow a format for framing jobs to be done, statements that are solution-agnostic, result in progress, and are stable across time (see Brian Rhea’s helpful article on this topic).

I’m doing something else and want to be entertained, informed, etc.

Podcasts certainly fit the bill here much of the time. Clubhouse adds something new and interesting in how lightweight the decision is to jump into a room and listen. With podcasts there’s a spectrum: on one end you have informative shows like deep dives on history or academic subjects (think Hardcore History or EconTalk) that demand attention and that entice you to completionism, and on the other, entertainment-centric ones for sports or movies, where you can lightly tune in and scrub through segments.

The spontaneity of Clubhouse rooms lends well to dropping in and listening in on a chat in progress. Because so many rooms tend to be agendaless, unplanned discussions, you can drop in anytime and leave without feeling like you missed something. Traditional podcasts tend to have an agenda or conversational arc that fits better with completionist listening. Think about when you sit down with Netflix and browse for 10 minutes unable to decide what to watch. The same effect can happen with podcasts, decision fatigue on what to pick. Clubhouse is like putting on a baseball game in the background: just pick a room and listen in with your on-and-off attention.

Ben Thompson called it the “first Airpods social network”. Pop in your headphones and see what your friends or followers are talking about.

I have an idea to express, but don’t want to spend time on writing or learning new tools

Clubhouse does for podcasting what Twitter did for blogs: massively drops the barrier to entry to participation. Setting up a blog has always required some upstart cost. Podcasting is even worse. Even with the latest and greatest tools, publishing something new has overhead. Twitter lowered this bar, only requiring users to tap out short thoughts to broadcast them to the world. Podcasting is getting better, but is still hardware-heavy to do well.

There’s a cottage industry sprouting up on Clubhouse of “post-game” locker room-style conversations following events, political, sports, television, even other Clubhouse shows. This plays well with the live aspect. Immediately following (or hell, even during) sporting events or TV shows, people can hop in a room and gab their analysis in real time.

Clubhouse’s similarities to Twitter for audio are striking. Now broadcasting a conversation doesn’t require expensive equipment, audio editing, CDNs, feed management. Just tap to create a room and notify your followers to join in.

I want to hear from notable people I follow more often

This one has been true for me a few times. With the app’s notifications feature, you can get alerts when people you follow start up a room, then join in on conversations involving your network whenever they pop up. I’ve hopped in when I saw notable folks I follow sitting in rooms, without really looking at the topic. For those interesting people you follow that you make sure to listen to, Clubhouse expands those opportunities. Follow them on Clubhouse and drop in on rooms they go into. Not only can you hear more often from folks you like, you also get a more unscripted and raw version of their thoughts and ideas with on-the-fly Clubhouse sessions.

I want to have an intellectual conversation with someone else, but I’m stuck at home!

Or maybe not even an intellectual one, just any social interaction with others!

This is where the timing of Clubhouse’s launch in April of last year was so essential to its growth. COVID quarantines put all of us indoors, unable to get out for social gatherings with friends or colleagues. Happy hours and dinners over Zoom aren’t things any of us thought we’d ever be doing, but when the lockdowns hit, we took to them to fill the need for social engagement. Clubhouse fills this void of providing loose, open-ended zones for conversation just like being at a party. Podcasts, books, and TV are all one-way. Humans need connection, not just consumption.

COVID hurt many businesses, but it sure was a growth hack for Clubhouse.

Future Jobs to Be Done?

Products can serve a job to be done in a zero- or positive-sum way. They can address existing jobs better than the current alternatives, or they can expand the job market to create demand for new unfulfilled ones. I think Clubhouse does a bit of both. From first-hand experience, I’ve popped into some rooms in cases when I otherwise would’ve put on a podcast or audiobook, and several times when I was listening to nothing else and saw a notification of something interesting.

Above are just a few of the customer jobs that Clubhouse is filling so far. If you start thinking about adjacent areas they could experiment with, it opens up even more greenfield opportunity. Offering downloads (create a custom podcast feed to listen to later?), monetization for organizers and participants (tipping?), subscription-only rooms (competition with Patreon?). There’s a long list of areas for the product to explore.

Where Does Clubhouse Go Next?

There’s a question in tech that’s brought up any time a hot new entrant comes on the scene. It goes something like:

Can a new product grow its network or user base faster than the existing players can copy the product?

This has to be at the forefront of the Clubhouse founders’ minds as their product is taking off. Twitter’s already launched Spaces, a clone of Clubhouse that shows up in the Fleets feed. That kind of prominent presentation to Twitter’s existing base adds quite the competitive threat, though Twitter isn’t known for it’s lightning-quick product innovation over the last decade. But maybe they’ve learned their lesson in all their past missed opportunities. What could play out is another round of what happened to Snap with Stories, a concept that’s been copied by justaboutevery product now.

Clubhouse is doing a respectable job managing the technical scalability of the platform as it grows. The growth tactics they’re using with pulling in contacts, while controversial, appear to be helping to replicate the webs of user connections. The friction in building new social interest graphs is one of the primary things that’s stifled other social products over the last 10 years. By the time new players achieve some traction, they’re either gobbled up by Twitter or Facebook, or copied by them (aside from a few, like TikTok). Can Clubhouse reach TikTok scale before Twitter can copy it?

There are still unanswered questions on how Clubhouse’s growth plays out over time:

How far can it reach into the general public audience outside of its core tech-centric “online” crowd?

Like any new network-driven product, when it’s shiny and new, we see a gold rush for followers. What behaviors will live chat incentivize?

How will room hosts behave competing for attention? What will be the “clickbait” of live audio chat?

What mechanisms can they create for generating social capital on the network? How does one build an initial following and expand reach?

Right now, the easiest way to build a following on Clubhouse is just like every other social network’s default: bring your already-existing network to the platform. It’s a bit early to see how Clubhouse might address this differently, but most of the big time users were folks with large followings on Twitter, YouTube, or elsewhere. It’d be cool to see something like TikTok-esque algorithm-driven recommendations to raise distribution for ideas or topics even outside of the follower graphs of the members of the rooms.

Clubhouse (and this category of live multi-way audio chat) is still in the newborn stages. As it matures and makes its way to wider audiences outside of mostly tech circles, it’ll be interesting to see what other “jobs” are out there unfilled by existing products that it can perform.

In many markets during COVID, startups have a host of advantages over their incumbent competitors:

Consequently, growth and innovation efforts are quickly deprioritized or even fully abandoned. Incumbents place their primary focus on stopping the decline of existing revenue streams rather than creating new ones. This mindset slows them down even more during crises and tethers them to mature and declining business models.

That’s why right now, startups have even more room to maneuver in and around (and even beyond) their bigger competitors than in “good” times. Startups can try more things without attracting a response or even being noticed. It also gives Founders time to iterate and test more, granting more runway for one of the holy grails of startups: product-market fit.

In his article “Strategy Under Uncertainty,” Jerry Neumann contrasts the traditional Porter model of business strategy with one more suited to startups, the former being modeled around mature organizations operating in known competitive spaces, the latter around startups moving in opaque environments with higher uncertainty and more moving parts.

In the piece he defines “strategy” as a framework for “how to make decisions in situations that are not yet known.” To have a purposeful, intentional approach to an objective, whether in war, sports, or business, you have to formulate a model for predicting the future. Without clarifying some future state you think will develop, it’s impossible to take the right series of actions to end in success.

Strategy in some businesses is all anyone wants to talk about. In others it’s taken for granted or not discussed enough explicitly. Each of these paths is incorrect.

In the second case, most anyone would acknowledge that little meaningful progress can happen in a business with no strategy. You’re merely subject to the whims of the environment and other players around you. You rely on getting lucky.

The first case, though, is also surprisingly common. In the modern business universe, being a “strategic thinker” is an accolade. The business literature surrounding us pushes this idea so much that in some environments, everyone wants to strategize. Without the right guidance and guardrails, this can go on far too long and can be actively detrimental to execution.

One of the dangers I see of over-strategizing in startup environments is that it tempts you into searching for information that may not be there in the first place. We think we can “map the competitive landscape”, but what if we can’t lay out an immediately clear picture? We begin to prioritize having a drawable diagram of our competitive landscape over the actual reality on the ground. In pursuit of having a legible map, we stretch definitions or cut corners. The map becomes the goal.

As Neumann points out, the environment in startups is riven with uncertainty and moving targets. You have more unstable dynamics than you’d find in many mature, large companies:

Startups operate as part of a complex system that encompasses not just their internal operations, but their customers, their suppliers, other companies that might compete or cooperate with them, financiers, the media, the government, and society at large. Each of these other entities also makes decisions, and the results of their decisions must factor into the startup’s decision model. The changes most likely to affect a startup are the ones that happen as a result of the decisions the startup itself makes, a complex feedback loop.

One of my core beliefs is that in spaces of high uncertainty, too much analysis and planning builds in more risk rather than less. Partially this is because of the time we spend in planning; more time spent equates to higher expectations and an inflated sense of what we know. I’ve analogized this situation to a high-wire act: the more assumption you make that your Big Prediction is correct, and the more you build toward that up front, the higher you raise that wire over the ground. As your predictions go farther into the future and your bets get bigger, the risk keeps rising.

Building strategy is so tempting. It always sounds like a good thing to spend time on, and it often is. Somewhat perniciously, it can be even more tempting in a startup environment, where the risk is high and the runway short. You perceive little margin for error, so you have to get the plan right.

The trouble is that there’s a limit to how much it can do for you in a startup. And the more novel your idea the higher the uncertainty as to what the future of the market holds. Bias creeps in about what you think you know about the predictability of the space; just because you’ve done n hours of analysis doesn’t guarantee you have any clearer an answer than at hour two. But human biases will tempt you to believe you’ve imbued it with more legibility than there really is. The only worse decision making environment than one with no information is one with actively misleading information.

Like many things, I believe the right way to approach strategy in startups is a nuanced middle.

You should always start with a clear vision of the future. What world is your business or product trying to create? How are you changing life for your customers or users? The answer to this question sets the course, but not the strategic roadmap, go-to-market, or many other things you need to figure out.

I like to think of strategy in medium term chunks. The goal is to build a hypothesis that we can push forward, rollout a strategy for, and test with real feedback on the order of weeks or months. More frequent, lower intensity strategy sessions that allow you to come up for air and work with real information about the world that you’ve learned, rather than speculating on your 5 year strategy at a whiteboard for a month.

Thinking you know more than you do leads to dangerous and risky plans. Usually it’s possible to know enough to take smaller, incremental steps based around much more reliable signal, with less interference from bias. There’s typically room for a couple of riskier moves here and there where you could earn outsized returns if you’re right. But the majority of the time, a tempered approach to just-right “Goldilocks” strategizing is the right way to go for a small team and a new product.

I rediscovered this great piece from Patrick McKenzie, an SEO primer for startups, but actually valid for anyone trying to generate traffic, interest, and business from the internet for anything at all.

The first cut of your SEO strategy will be wrong, just like v1.0 of your product will be non-responsive to the needs of your users. That is OK: after you start you’ll begin collecting insights and data which let you refine it. You want to get something out the door as soon as possible so that you can begin collecting links, other indicia of trust, and data on what is working for you. Many startups wait until launch to put a significant amount of content on their websites. This is almost always a mistake.

SEO has always been a powerful tool for us as we’ve expanded. We’ve used many of the approaches Patrick outlines here over the years to build a nice presence. I’d add my biggest takeaway here in getting impact out of SEO (and content in general) is to make it programmatic — it’s not something you do in spikes, except for things like major product release milestones or equivalent, but that you keep constant pressure on over time to gradually raise the waters. I strongly agree with the quote above, that if you treat content generation like an experimental, “agile” process, the error correction feedback it affords is priceless to be getting your work out there early. Time is your friend with exposure on the internet. The longer you have something up, the more opportunity for discovery.

For a 10 year old article, I can’t find anything in here that’s outdated or been made irrelevant.

Biologist Stuart Kauffman on biological functions and the “adjacent possible”:

The unexpected uses of features of organisms, or technologies, are precisely what happens in the evolution of the biosphere and econosphere, and the analog happens in cultural evolution with the uses of mores, cultural forms, regulations, traditions, in novel ways. In general, these possibles are novel functionalities, in an unbounded space of functionalities, and so are not mathematizable and derivable from a finite set of axioms.

A Joel Spolsky classic from 2002. Take advantage of the time you have when you’re independent, small, and lean. Don’t get hung up on grand strategic chess-piece moving, sitting still while you plan your Big Moves. A reminder to just keep pushing forward every day:

Fire and Motion, for small companies like mine, means two things. You have to have time on your side, and you have to move forward every day. Sooner or later you will win. All I managed to do yesterday is improve the color scheme in FogBugz just a little bit. That’s OK. It’s getting better all the time. Every day our software is better and better and we have more and more customers and that’s all that matters. Until we’re a company the size of Oracle, we don’t have to think about grand strategies. We just have to come in every morning and somehow, launch the editor.

There was a Twitter discussion going on this week around this piece, wherein Aaron Harris makes the case for seed stage companies to raise just enough money to find product-market fit, and not be tempted to greatly extend runway for experimentation:

I realized that the conversation about raising always anchors back to the idea of adding “months of runway.” That always seemed appropriate to me because it was a measure of the amount of time a company had to stay alive. Staying alive seemed good since it increased the time a company had to find product market fit and to grow.

But I now realize that this is the wrong framing because simply staying alive is an inadequate goal for a company. Founders start companies to find product market fit and grow. Venture capital is designed to speed growth, not to extend runway.

A new piece from Andy Matuschak and Michael Nielsen (beautifully illustrated by Maggie Appleton). Can we make reading a more engaging and interactive learning experience? This builds on previous ideas from the authors on spaced repetition.

Interesting take from one of Byrne Hobart’s recent newsletters. Contrasting a typical “full-stack” model of company-building and VC funding to a “sumo” model:

The amount of VC funding has been rising steadily, and returns are skewed by a few positive outliers, so any fund that doesn’t have a specific size mandate is actively looking for companies that can absorb a lot of capital as they grow. The best way to get more capital is to move from a capital-efficient business to a capital-inefficient one, so there’s a strong incentive to pivot in this direction.

The incentive is sometimes too strong. Some companies go beyond the “full-stack” model to what I think of as the “sumo” model: raising an intimidating amount of money just to scare off everyone else. The sumo model does prevent one failure mode for startups: the situation where every time Company A raises a round, it validates the model and lets Company B raise more, which forces Company A to burn through their marketing budget faster and raise an even bigger round, and so on until the entire space is over-capitalized and everyone’s assumptions about long-term unit economics are implausibly optimistic. It’s an easier strategy to try when capital is abundant, but it’s a harder strategy to pull off; the bar for “an absurd amount to invest in a company that just does X” keeps going up.

In the arena of geeky digital marketing, this is a great deconstruction of organic optimization tactics in play at Canva, one of the best out there at enabling discovery through search and backlink traffic. I love how thoughtful and intentional their page architecture is; it enables so much adaptive targeting to sweep up long-tail keyword spaces.

Every cherished mistaken assumption has a dead zone of unexplored ideas around it. And the more preposterous the assumption, the bigger the dead zone it creates.

There is a positive side to this phenomenon though. If you’re looking for new ideas, one way to find them is by looking for heresies. When you look at the question this way, the depressingly large dead zones around mistaken assumptions become excitingly large mines of new ideas.

I always enjoy conversations with Marc Andreessen and Ben Horowitz. This interview (conducted by Slack founder Steward Butterfield) reviews their experiences as founders back in the pre-bubble era and compares and contrasts that thematically with the tech landscape today.

This post from Eugene Wei has been making the rounds in tech. It’s a lengthy article dissecting how status is really the secret currency of success for social products — not individual utility or entertainment. He draws some interesting parallels between social networks (as status-building entities) and cryptocurrency ecosystems. Just like with crypto exchanges, “proof of work” is an essential prerequisite for success on a social network:

Why does proof of work matter for a social network? If people want to maximize social capital, why not make that as easy as possible?

As with cryptocurrency, if it were so easy, it wouldn’t be worth anything. Value is tied to scarcity, and scarcity on social networks derives from proof of work. Status isn’t worth much if there’s no skill and effort required to mine it. It’s not that a social network that makes it easy for lots of users to perform well can’t be a useful one, but competition for relative status still motivates humans. Recall our first tenet: humans are status-seeking monkeys. Status is a relative ladder. By definition, if everyone can achieve a certain type of status, it’s no status at all, it’s a participation trophy.

It’s an apt metaphor to think about social capital, its build-up, transference, and investment like that of financial capital:

I can still remember posting the same photos to Flickr and Instagram for a while and seeing how quickly the latter passed the former in feedback. If I were an investor or even an employee, I might have something like a representative basket of content that I’d post from various test accounts on different social media networks just to track social capital interest rates and liquidity among the various services.

Tweet “liquidity” is a great way to think about it:

In an effort to increase engagement, Twitter has, over the years, become more and more aggressive to increase the liquidity of tweets. It now displays tweets that were liked by people you follow, even if they didn’t retweet them, and it has populated its search tab with Moments, which, like Instagram’s Discover Tab, guesses at other content you might like and provides an endless scroll filled with it.

It’s a very long breakdown, but overall one of the best comprehensive pieces on what makes social networks tick and how network effects work.

This post from Hiten Shah tells the backstory of one of the more interesting startups these days, Airtable. Like the title states, the objective of Airtable is to build a no-code system for data management and application-building. At a billion-dollar valuation now, they’ve clearly knocked it out of the park with their product-led growth strategy.

Even in the face of the 5,000 pound gorilla of Excel, they’ve broken things open and are beginning to attract mass-market users.

Microsoft had been the undisputed king of productivity software for 20 years by the time Airtable went into development in 2012. What Microsoft––and virtually every other software company in the world––had failed to do was create a new spreadsheet product that people wanted to use. The ubiquity of Microsoft Office guaranteed Excel’s “success,” but it was stagnating as a product. Aside from some relatively minor performance updates and a handful of newer features, Excel looked and felt much the same as it did when it launched in the early ’90s. Microsoft’s Access had fared a little better (for a 26-year-old product) but was still aimed squarely at database administrators who possessed the programming and scripting skills necessary to work with SQL databases.

When I first heard about his company Opendoor (a real estate startup with the goal of creating faster liquidity for home sellers), I started following Keith Rabois. His Twitter account is a good follow.

This discussion covered topics as diverse as his political views, his original ideas for his companies, and investing principles.